The House of Chris Hohn: TCI Fund Management

TCI’s Market Value Has Risen $15 Billion in 135 Days

This piece had been sitting in my drafts for months, and the final push to publish came after reading Rupak Ghose’s excellent essay,

While I won’t pretend to match Rupak’s flair, what follows is my own attempt to add to the growing body of literature on the remarkable man behind TCI—shaped by interviews, conversations with mutual friends, and years of watching his work.

Christopher Hohn’s TCI Fund Management has added $15 billion in market value in just 135 days. That’s a 43% rise since December 31st, taking the total to over $50 billion—all in a portfolio with close to 73% concentrated in just five core holdings. GE Aerospace alone accounts for $10.7 billion, with Moody’s, Microsoft, Canadian Pacific, and Visa rounding out the top tier.

While others chase themes, Hohn compounds certainty. With a portfolio turnover of just 21.4% and an average holding period that rivals some marriages, TCI doesn’t trade. It owns. The result? A percentile rank of 98 by AUM, and a track record that forces even the loudest managers to fall silent.

This is not performance by luck or leverage. It’s precision, applied over decades. TCI’s numbers are staggering—but they are not the story. The story is how they came to be.

I've always had an admiration for Sir Chris. Not the kind of admiration that blooms from distance or mystique, but the kind that grows from studying someone deeply—line by line, decision by decision, year over year—until you recognize in their architecture of thought something unmistakably rare. In a world where fund managers court style over substance and market cycles flush out convictions like weak foundations in a flood, Chris Hohn has built a fortress of intellectual clarity. Not loud. Not promotional. But fiercely principled, ruthlessly consistent, and astonishingly effective.

If you’ve ever tried to decode what separates great investors from the merely good, you’ll likely encounter detours filled with noise: charm, charisma, pedigree, even luck. What you will rarely find—and what Sir Chris offers in abundance—is philosophical coherence applied with surgical execution. His is not a mosaic of ideas; it's a single mosaic tile, perfected.

At TCI, the oxygen of investment isn’t growth, or novelty, or narrative—it’s the moat. Not figuratively. Not aspirationally. But clinically. If there’s no high, sustainable barrier to entry, the conversation ends before valuation even begins. Moats aren’t accessories; they’re prerequisites. Substitution and competition are not mere risks—they are existential threats. Hohn doesn’t flirt with fragility. He hunts indomitability.

You see it in his lens on infrastructure: airports like Aena, toll roads, electricity transmission lines—physical monopolies that aren't just hard to replicate; they are economically irrational to replicate. But that’s only the entry point. Even among monopolies, regulation remains the knife that can carve away value. That’s why TCI doesn’t generalize. Every case is dissected. Take the nuance of dual-till regulation at Aena. It’s these seemingly minor details—often missed by fast money—that transform a good asset into a great one.

Then there’s his appreciation for advanced intellectual property—where engineering complexity creates temporal moats few even understand, let alone breach. Aircraft engines are a canonical example: thousands of parts, metallurgical alchemy, safety tolerances forged over decades, and service contracts that spin into lucrative installed base economics. The complexity is the moat, and time itself becomes a barrier to entry. No startup, no SPAC, no garage disruptor is coming for that turf.

But moats don’t always wear steel or software. Sometimes they wear scale. Sometimes they are embedded in switching costs so painful that customers will tolerate mediocrity to avoid the agony of transition. Think mission-critical software, the kind that, once embedded, becomes the neural wiring of an organization. Or look at Microsoft: a firm whose bundling genius with Teams defeated technically superior offerings like Zoom, not through engineering, but through inertia and ubiquity.

What’s particularly interesting is how Hohn doesn’t get seduced by recurring revenues unless they come attached to essential services. It’s not about how often the customer comes back, but whether the customer can afford not to. Moody’s is a case in point. You can defer getting your debt rated, but eventually the debt market calls your bluff.

This brings us to his quiet disdain for certain industries—banks, insurance, traditional asset managers, wireless telecom, airlines. Not because these sectors lack brains or bravado, but because they lack what Hohn demands above all: predictable earnings power underpinned by enduring moats. He has little patience for sectors where opacity, leverage, or commoditization infect the economics. Banks, in his words, suffer from structurally low-quality earnings, obfuscation, and agency risks that can implode shareholder value overnight. And unlike many in the buy-side fraternity, he doesn’t believe in ‘value traps’ dressed up as cheap: he’s not tempted by broken businesses selling at 50 cents on the dollar. If earnings power is unknowable or unprotectable, it’s not value—it’s delusion.

Then there’s his view on growth: beautifully unfashionable. Growth is not the answer unless it’s accompanied by fortress-level pricing power. And even then, he reminds us, pricing power is the rarest element in the investing periodic table. If you find it, and it flows through cleanly to profit, you’ve found leverage in its purest form. Especially in lower-margin businesses, that last 3% of incremental price could be the difference between a dud and a diamond.

But it is the sequence—the discipline of process—that makes TCI more than just a vehicle of preferences. Hohn doesn’t let valuation seduce him early. The financial model is irrelevant if the moat doesn’t pass inspection. The due diligence goes deep and wide: not just numbers, but reputational audits, reference checks with ex-competitors, off-the-record conversations with former CEOs. What you won’t see is over-reliance on management teams. Unlike the romanticism of founder worship that’s gripped venture and growth investing, Hohn understands that great capital allocators don’t need to be best friends with the executives—they need to out-think them.

This refusal to bend to market fads has made TCI an outlier. And that’s the irony: the firm’s brutal insistence on investing only in the irreplaceable has itself become irreplaceable in a world drunk on disruption. The strategy is concentrated, conviction-led, and almost stubbornly non-consensual. But it works. Year after year, decade after decade, compounding quietly.

There are no celebrations, no screaming from CNBC balconies. Just a relentless pursuit of quality, moated compounders bought with care and sized with aggression. It’s the opposite of modern investing fashion. Which is perhaps why it will outlast it.

In the end, what Sir Chris teaches us is not just how to invest, but how to think. He invites us to imagine a market where capital flows not toward the noisy, but toward the necessary. A market where risk is not abstract, but measurable in competitive physics. A market where excellence is not spoken—it’s proven.

And in that world, the moat is king.

Further Reading: How Sir Chris Invests—The Full Framework

For those who prefer technical structure and want to study the core principles directly, the following learning sheet synthesizes Sir Chris Hohn’s investment framework, based on public interviews, conversations with mutual friends, and the operating principles of TCI Fund Management. It distills decades of thinking into a rigorous model—designed not just to explain what works, but why.

Learning Sheet: Investment Principles & Practice from Sir Chris Hohn (TCI Fund Management)

I. Core Investment Philosophy: The Paramount Importance of Barriers to Entry (Moats)

Rejection of Common Focuses:

Growth alone is not sufficient.

Newness alone is not sufficient.

The Essential Criterion: High, sustainable barriers to entry ("moats") are the most important factor, without which TCI typically does not invest in the style of investing they pursue.

Function of Moats:

Make the business difficult to replace (mitigate substitution risk).

Make the business difficult to compete with (mitigate competition risk).

Consequences of Lacking Moats:

Competition kills profits.

Substitution eliminates the business.

Caveat on Low-Quality Assets: Investing in cheap, average/low-quality assets trading at significant discounts to replacement cost can work (distressed real estate example), but Hohn lacks confidence in this approach due to the unpredictability of earnings power in such businesses.

II. Identifying and Analyzing Moats

Requirement: Moats must be sustainable. Ideally, a business possesses multiple moats.

Specific Moat Categories Identified:

Irreplaceable Physical Assets (Infrastructure): Natural monopolies difficult or impossible to replicate due to planning, land, or economic case.

Examples: Airports (Aena - natural monopoly, planning difficulty), Toll Roads, Railroads, Telecom Towers, Electricity Transmission Towers (Red Electrica example).

Nuance: Must analyze case-by-case (e.g., cable infrastructure can be overbuilt). Regulation needs careful consideration (see below).

Advanced Intellectual Property (IP): Highly complex, difficult to replicate.

Example: Aircraft Engines (materials complexity, operating temps, thousands of parts, few players, no new entrants for 50+ years, reliability trumps price).

Installed Base: Creates follow-on business.

Example: Aircraft Engines (spare parts).

Scale: Provides competitive advantage, though not a guarantee on its own.

Network Effects: Value increases with more users. Can lead to "winner takes all" dynamics.

Examples: Visa, Meta, Marketplaces/Exchanges with liquidity (Deutsche Borsa/Eurex, LSE/LCH Clearnet, CME). First-mover advantage can be key in establishing this.

Strong, Sustainable Brands: Some brands have lasting value, but not all.

Example (briefly): McDonald's.

Customer Switching Costs: High costs (economic, operational, or technical) make customers reluctant to switch providers.

Example: Mission-critical software (complexity). Microsoft Office Bundle (bundling creates switching costs, installed base advantage allowed distribution of Teams, "good enough" and free distribution can defeat technically superior products like Zoom).

III. Evaluating Business Quality Beyond Moats

Essential Product/Service: More important than the predictability of when revenue recurs. Avoids discretionary demand.

Example: Rating Agencies (Moody's) - Issuers can defer, but debt must eventually be refinanced and rated (essential need).

Revenue Quality:

Prioritize essential products/services.

Recurring revenue streams are generally positive.

Growth (Nuance):

Growth is less important than moats. Profitless growth exists (airlines example).

Growth can come from Volume and Price.

Pricing Power (Crucial): The ability to price above inflation is a key test of a strong moat (Buffett's test).

This is rare but highly valuable.

Incremental pricing is largely profit (high flow-through to earnings).

Potent leveraged effect on profits, especially for lower-margin businesses.

Capital Intensity: Part of the equation, influences the value of growth. Businesses with low capital intensity requirements for growth (like unregulated parts of airports) are highly attractive. Returns on capital are important.

Regulation (Risk Factor):

Low barriers: Competition/substitution risk.

High barriers: Regulatory risk (regulators "come knocking").

Ideal: Competition exists but is weak and rational ("apparent competition").

Mitigation: Detail matters (e.g., dual-till regulation in airports like Aena differentiates value).

IV. Industries and Business Models to Avoid

General Principle: Highly competitive industries, prone to disruption by existing players or new technologies. Investors tend to underestimate these forces.

Specific Examples (Considered "Risky and Bad"):

Banks: Low quality of earnings, high leverage (often exceeding stated equity/RWA ratios when considering total assets), opaque balance sheets, significant agency problems (risk of incompetent management destroying shareholder value for short-term gain, e.g., Anglo Irish, Bear Stearns).

Auto Industry (Commodity)

Retail (Commodity)

Insurance

Commodities

Commodity Manufacturing

Most Manufacturing

Traditional Asset Managers

Fossil Fuel Utilities

Airlines

Wireless Telecom

Media

Advertising Agencies

V. Investment Process and Valuation

Sequencing: Do not look at valuation until comfortable that barriers are strong and the business will survive long-term.

Due Diligence (Beyond Financials):

Reference Checks: Speak to relevant industry participants, including former competitors/CEOs, to validate thesis and uncover blind spots. (Aircraft engine example).

Management Assessment: Important, but not critical if the underlying assets/moats are strong enough. Ideally done through meetings.

Competitor Insights: Understand their perspective.

Competitive Landscape: Analyze peer companies.

Track Record: Review the company's history.

Assumption of Incomplete Information: Recognize you won't understand everything initially; discoveries often involve negative findings.

Team Debate: Discuss internally, actively seeking competing views (especially "bear" cases, technology disruption risks, competition analysis).

Valuation Approach:

Uses various metrics (P/S, Cash Flows, DCF).

Discounted Cash Flow (DCF): Most important tool for long-term valuation.

Value is disproportionately weighted towards later periods for great companies.

The ability/willingness to model and hold for the long term (8+ years average holding period) provides an analytical and behavioral edge.

Intrinsic value compounding over the long term matters more than multiple fluctuations over the short term (Moody's example: consistent earnings growth over 100 years means even buying back stock at higher multiples was value-creative).

Multiples: Matter to a point, but less than growth when viewed over very long horizons.

Intrinsic Value Certainty: Acknowledges intrinsic value estimation is approximate, not an objective truth. Forecasting uncertainty increases over longer horizons.

Simpler Tests: For businesses with extremely strong moats (like airports/toll roads), asking "Will the business still be around in 30 years?" is a valid, simpler test.

Conviction (Beyond Value): Investment decisions require not just attractive value but also high conviction ("sufficiently obvious" thesis, "sleep at night" test). Conviction levels are higher for businesses with strong physical assets and low substitution risk (toll roads vs. retailers). Permanent loss of capital is the ultimate risk to avoid.

VI. Portfolio Management and Strategy

Long-Term Holding Period: TCI's weighted average holding period is 8 years. This stems from a "private equity approach" mindset – buying with the intention to hold indefinitely ("forever"), as market prices may be unfavorable if forced to sell at a specific time.

Concentration: High conviction leads to concentrated positions (e.g., 10% position size, 10-15 stocks in total).

VII. Market Structure and Opportunity

Public vs. Private Markets: Belief that there are more genuinely "good" companies in the public markets, especially among the largest capitalized companies (Top 100 public > Top 100 private).

Reasoning for Public Market Superiority (for Top Tier):

Large companies have resources (money, R&D) and scale to compete effectively and often crush smaller innovators (Zoom/Microsoft example).

Incumbency and switching costs benefit large, established players.

Size excludes private equity from acquiring the largest, potentially highest-quality businesses (Visa example).

When public companies sell assets to private equity, they often offload non-core or less-attractive businesses.

VIII. Activism and Engagement

Activism Spectrum: Ranges from aggressive board/CEO removal and forced sales to softer, constructive dialogue and engagement.

Evolution of Approach: TCI has shifted from aggressive tactics (ABN AMRO example - profitable but fundamentally flawed business, forced sale but buyers failed) to more constructive engagement.

Challenges of Hardcore Activism Today: Difficult to succeed due to the dominance of passive investors (index funds) who are hard to mobilize for voting. Active share base is smaller than in the past.

Current Approach: Act as owners. Be interested, engaged, assert legal rights (e.g., board representation).

Governance: Learned that governance does matter.

Motivation for Aggressive Action (Now Rare): Typically reactive, when an existing holding undertakes value-destructive actions (Saffron/Zodiac example - high price, share payment when TCI believed stock was undervalued, forced price cut and cash payment via aggressive campaign including litigation threat and shareholder vote demand).

Personal Toll: Engaging in aggressive fights and litigation is stressful ("not for the faint-hearted"), even if ultimately successful. Hohn no longer enjoys fighting; it's done when necessary to protect investment ("fighting for my life").

IX. Shorting (Asymmetric Risk)

General View: Shorting is "not a great business."

Core Problem: Can be "right" on the fundamental thesis but be unable to hold the position or fund losses if the stock price moves against you in the short/medium term (unlimited theoretical downside).

Investor Psychology: Understanding how market sentiment and irrationality can sustain overvalued/fraudulent companies is difficult. Buffett and Munger found it too hard.

Wire Card Example:

Recognized accounting "red flags" (small auditor, lack of cash flow, empty offices for key businesses).

Journalistic work (FT) provided key public information.

Needed independence of thought despite German establishment support for the company.

CEO meeting reinforced skepticism ("pathetic demonstrations of technology").

Recognized it became a "confidence game."

Filed criminal complaint for fraud (as activist short) to force action and avoid appearing manipulative if not public; this created chaos and forced investigation.

Illustrates the risk: Stock initially rose after report was dismissed; required conviction and ability to withstand adverse price movement.

Confirms the difficulty: Even with clear evidence of fraud ("in plain sight"), the market/establishment can support the company for extended periods.

X. Organizational Culture and Hiring

Team Size: Small investment team (7-8 people).

Culture: Collegiate, built on intangible trust.

Reason for Small Size: Best people value the human aspect and environment over larger, potentially impersonal structures. Protects culture. Senior team blessing required for new hires.

Hiring Criteria:

Share the investment philosophy.

Demonstrate competence through case studies.

Desire to work collaboratively in a team.

Ability to "get along" with others.

Open-mindedness and lack of dogmatism (willingness to be wrong). Personality matters.

XI. Personal Philosophy and Philanthropy

Philanthropy Origin: Early intuition led to donating a large bonus; understanding evolved over time as a "soul urge" – the fundamental essence/consciousness seeking service and helping humanity.

View on Money: Does not care about personal accumulation; value is in its ability to help others. Gives away everything earned.

Spiritual Perspective: Believes the spiritual world is real and the soul/consciousness is the true essence, not just personality/body. Service is the source of real purpose, meaning, and joy. Crises (death, disease, divorce) can trigger inward reflection and this realization. Does not necessarily believe in only one life.

Upbringing Impact: Working-class background and immigrant father fostered independence of thought (as an outsider), work ethic, and desire to achieve.

Foundation Focus Areas (Examples):

Climate Change: Building movement infrastructure, advocating for regulation (technical assistance to governments, focus on high-emission growth regions like Asia), tax reform (remove fossil fuel subsidies, advantage clean tech), methane reduction, environmental litigation.

Children's Health (Africa/India): Foundational issues like contraception access/agency neglected tropical diseases (Trachoma surgery, $50 prevents irreversible blindness), HIV/AIDS. Highlights the immense leverage of small philanthropic capital in these areas compared to discretionary spending.

View on ESG Backlash: Sees it as a "dark" phenomenon prioritizing short-term profit ("burn down the planet") over future generations and vulnerable populations, stemming from a lack of evolved consciousness and identification solely with the material/personality rather than shared humanity/service.

XII. Advice for Young People

Engage in a spiritual path/study.

Recognize the spiritual world is real and the soul is not a myth.

Understand that consciously connecting to this inner essence (via various paths, including suffering) is the source of real purpose, meaning, and joy, making other life challenges easier.

As always, thank you for reading.

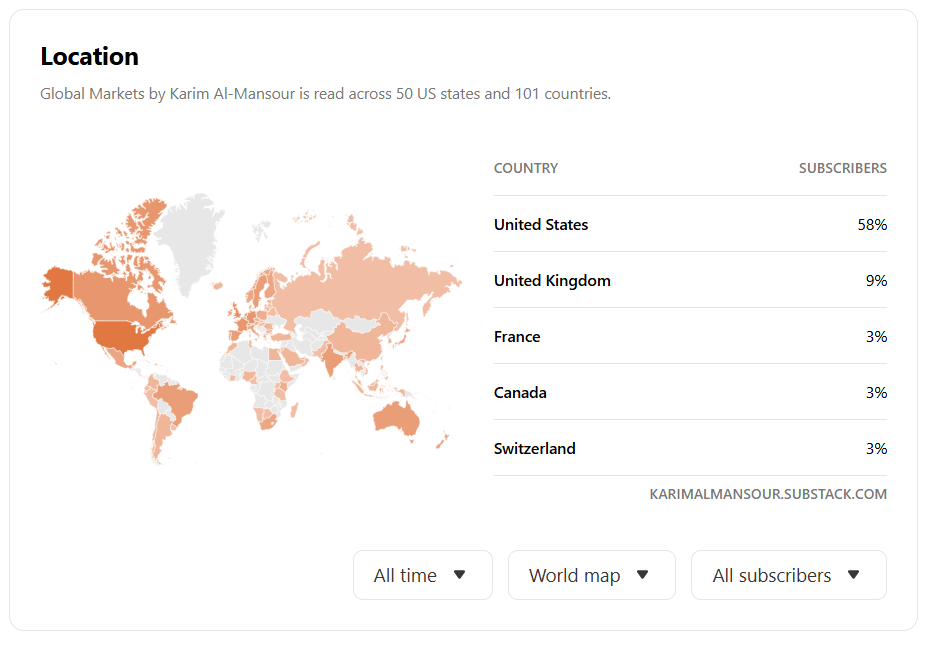

As we continue exploring the complexities of global markets together, I’m genuinely humbled by the growth of this community—now 56,000+ strong. It’s an honor to engage with such an insightful and globally diverse audience, with readers spanning 101 countries, from the United States to Switzerland.

Your feedback and engagement have been instrumental in shaping the topics I explore. If you've found value in these perspectives, I’d love for you to share this newsletter with your networks. Together, we’re fostering deeper discussions and critical thinking about where the markets are heading. Please write to me at kam@amanahcapital.uk